Redefining value: Climate transition and the future of GCC chemicals

Faced with emissions-intensive value chains and a deep reliance on hydrocarbons, the chemical industry stands at a climate crossroads. The challenges of the climate transition are immense – but so is the opportunity to lead.

Nowhere is this potential more pronounced than in the GCC, where record-breaking investments in renewables, green hydrogen, and bold national strategies are laying the foundation for a reimagined value creation model.

The real question? How can companies reframe climate transition risks as strategic levers, and embed climate alignment at the core of business performance and decision-making?

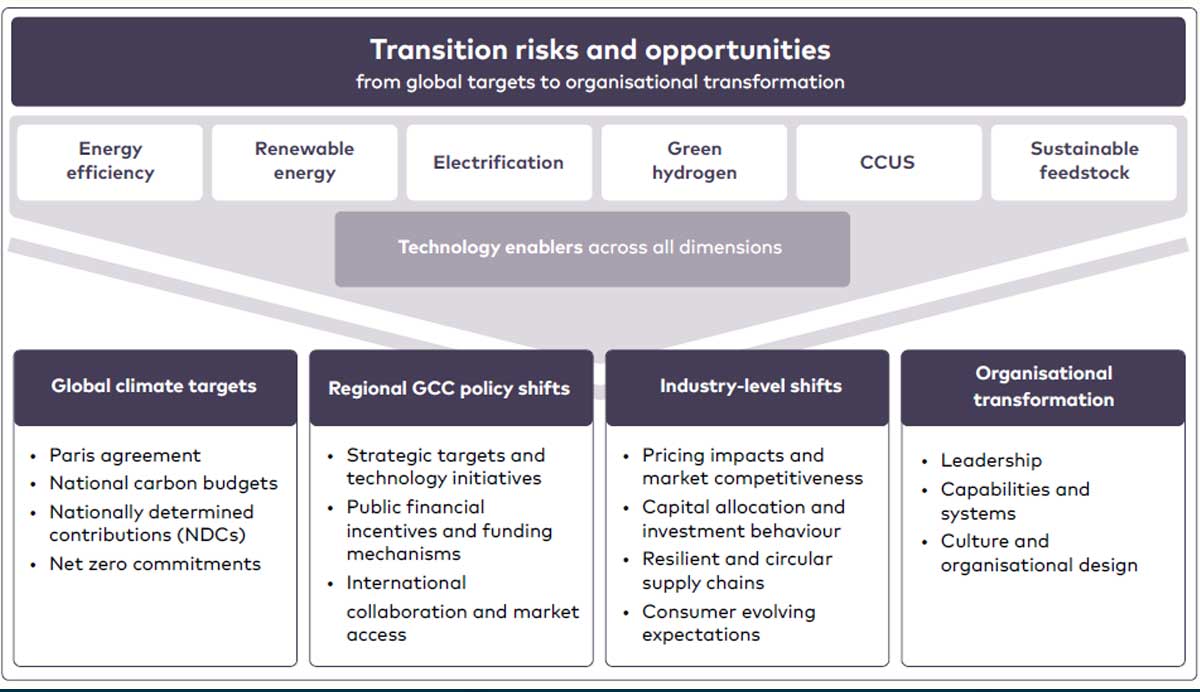

Figure 1: Structural view of how transition drivers interact, anchored in technologies that catalyse progress across levels

The answer lies in connecting five forces (Figure 1) – enabling technologies, global climate targets, regional policy signals, industry shifts, and organisational transformation – into a unified strategy. Done well, this can future-proof chemical players against disruption and set them apart in an increasingly carbon-conscious market.

Why the chemical industry is under pressure

The chemical industry emits over 3 billion metric tons of CO2 equivalent each year. This is 5-6% of all global emissions, making the sector the third largest industrial emitter behind cement and steel. In fact, the seven primary chemicals account for nearly half of these emissions.

The challenge is producing more with less emissions especially as demand for these products is rising with global population growth.

For chemicals, this challenge is amplified. The use of hydrocarbons as both energy source and chemical feedstock means chemicals face more constraints in reducing emissions compared to other industries. Renewables and electrification can decarbonise emissions from energy use, but replacing fossil-based feedstocks that produce core chemical products is far more complex.

The chemical industry emits over 3 billion metric tons of CO2 equivalent each year – 5-6% of all global emissions

This complexity sharpens the urgency to transition. The International Energy Agency’s (IEA) Net Zero Roadmap calls for reducing primary chemicals emissions by 95% to just 65 million metric tons of CO2 by 2050. Reaching it will require technologies and business models to transform at scale quickly.

For GCC companies, rather than only reacting to global pressure, proactively shaping the future of low-carbon chemicals can create a global competitive advantage.