How risk and resilience reshape PE investment in high-risk industries

Private equity investment in high-hazard industries is entering a new phase. Deals are fewer but larger, capital is concentrating in scaled assets, and operational resilience is becoming a key driver of value creation. As volatility, climate disruption and regulatory pressure reshape the operating landscape, investors are looking beyond financial engineering. What truly determines whether an asset sustains-or erodes-value over a 7-10 year hold? This report combines PitchBook data and dss+ insights to explore the factors redefining PE investment in these sectors.

Why private equity is doubling down on high-risk industries

Private equity (PE) firms are uniquely positioned to transform mature, volatile, and high-risk industries. With ownership periods spanning several years and in some cases decades, PE firms invest for the long haul and are no stranger to capital-intensive operations. Mining, energy refining, and chemicals are among just some of the sectors that are increasingly being identified by PE firms as targets for value creation and consolidation.

PE dealmaking in these industries is becoming more concentrated and selective, with fewer but larger transactions driving aggregate value. Record average deal sizes and outsized exits reflect conviction in long-term demand, but they also heighten execution risk and concentrate fund performance in a smaller set of scaled assets.

Commodity price volatility directly shapes cash flows and investment timing across these areas. Firms may view this exposure as an opportunity to acquire assets at favorable valuations, apply operational discipline to stabilize performance if needed, and create scaled platforms for greater returns once prices normalize.

Structural flexibility in dealmaking signals risk management rather than retreat. Sponsors are leaning into growth investments and add-on strategies-particularly in the energy and metals & mining industries-to balance exposure and competitive positioning in volatile markets.

“Resilience is not a one-and-done underwriting; it is an operating capability that determines whether value compounds or erodes over the hold period.”

- Chris Afors, Global Head of Strategy and Global Head of Private Equity & Principal Investors at dss+

Geopolitical uncertainty and new demand for the materials and infrastructure that enable artificial intelligence (AI) technologies is having an outsized effect on the dealmaking landscape. Operational and strategic risk management are more critical than ever to ensure resilience, and private investors are adjusting their own strategies in response.

Resilience is largely a capability built through post-transaction operating discipline. Assets that sustain cash flow and cost positioning, tight compliance, and operational reliability are increasingly differentiated over time. Tightening regulatory constraints, financing bifurcation, and climate-driven disruptions are the primary underestimated signals that shape outcomes in heavy industrial sectors. Throughout this report, dss+ experts weigh in on critical considerations for firms assessing and operating in these sectors.

Similar to dealmaking trends, exit markets are increasingly held up by a limited number of larger transactions. This dynamic raises the bar for operational discipline, capital governance, and resilience for portfolio companies as investors seek proportionate returns over extended holding periods.

“Resilience can no longer sit at the periphery of the value creation plan.”

- Panagiota Kovani, Senior Manager, Private Equity & Principal Investors Practice at dss+

Capital concentration and valuation expansion outweigh volume softness

One major industry-agnostic trend unfolding in private capital markets is that of capital concentration. Fewer deals are closing, and fewer new capital commitments are being made for funds. Major deals are still closing, but for a more select number of players compared with the early 2020s.

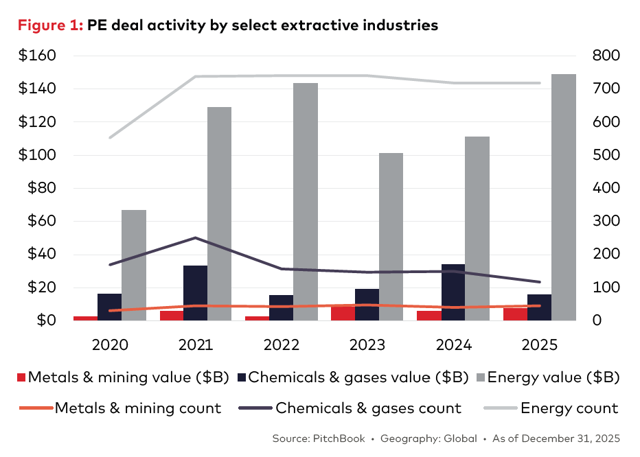

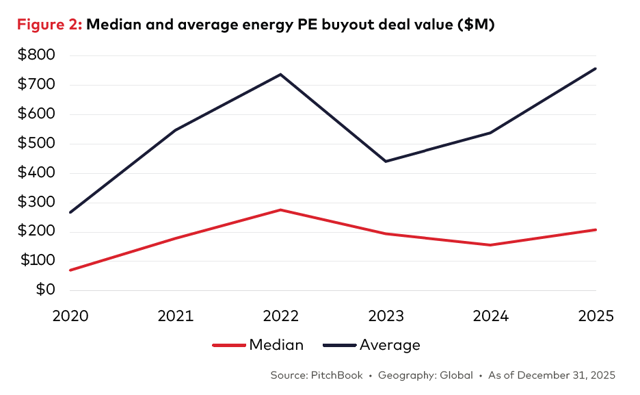

Across extractive industries, capital concentration trends are taking shape as firms make a limited number of outsized investments in priority areas. A full rebound to the pace of investments made in the pre-pandemic era remains on the horizon, indicating a confident but uneven outlook (Figure 1). The average buyout size in the energy industry, for example, rose more than 40% in 2025 to a record $756.9 million (Figure 2).

“Longer ownership raises the bar on organisational capability. Sponsors must build teams capable of multiyear transformation.”

- Alex Krause Principal, Private Equity & Principal Investors at dss+

*No registration is required.

Authors

As a Senior Manager at the Private Equity Practice within dss+, Panagiota leads the work with private equity clients, supporting funds, firms, and their portfolio companies across the full PE lifecycle. She focuses on helping investors strengthen operational performance and value creation, bringing a deep understanding of how operational risk, excellence, and sustainability drivers shape investment decisions, transformation, and exit readiness. Panagiota's previous experience spans across management consulting and financial services with deep expertise in operational risk management, operational excellence and digital enablement.

As Principal within the Private Equity EMEA at dss+, Alex brings more than 20 years of international leadership experience across management consulting and industry. He works with private equity firms and portfolio companies on operational due diligence, value creation and large‑scale transformations, with deep hands-on expertise in operations, supply chain and ORM. Prior to joining dss+, he was a director in the operations and supply chain practice of a global consulting firm, leading teams and programmes across energy, industrial manufacturing, pharmaceuticals, logistics, and aerospace and served as programme manager at a major utilities company.

As a Senior Manager at the Private Equity Practice within dss+, Panagiota leads the work with private equity clients, supporting funds, firms, and their portfolio companies across the full PE lifecycle. She focuses on helping investors strengthen operational performance and value creation, bringing a deep understanding of how operational risk, excellence, and sustainability drivers shape investment decisions, transformation, and exit readiness. Panagiota's previous experience spans across management consulting and financial services with deep expertise in operational risk management, operational excellence and digital enablement.

As Principal within the Private Equity EMEA at dss+, Alex brings more than 20 years of international leadership experience across management consulting and industry. He works with private equity firms and portfolio companies on operational due diligence, value creation and large‑scale transformations, with deep hands-on expertise in operations, supply chain and ORM. Prior to joining dss+, he was a director in the operations and supply chain practice of a global consulting firm, leading teams and programmes across energy, industrial manufacturing, pharmaceuticals, logistics, and aerospace and served as programme manager at a major utilities company.

As a Senior Manager at the Private Equity Practice within dss+, Panagiota leads the work with private equity clients, supporting funds, firms, and their portfolio companies across the full PE lifecycle. She focuses on helping investors strengthen operational performance and value creation, bringing a deep understanding of how operational risk, excellence, and sustainability drivers shape investment decisions, transformation, and exit readiness. Panagiota's previous experience spans across management consulting and financial services with deep expertise in operational risk management, operational excellence and digital enablement.

As Principal within the Private Equity EMEA at dss+, Alex brings more than 20 years of international leadership experience across management consulting and industry. He works with private equity firms and portfolio companies on operational due diligence, value creation and large‑scale transformations, with deep hands-on expertise in operations, supply chain and ORM. Prior to joining dss+, he was a director in the operations and supply chain practice of a global consulting firm, leading teams and programmes across energy, industrial manufacturing, pharmaceuticals, logistics, and aerospace and served as programme manager at a major utilities company.